“Low Price, High Potential: Understanding the Investment Prospects”

In the dynamic world of investing, making sound decisions can be both exciting and challenging, especially when it comes to analyzing companies with promising potential but facing certain uncertainties.

One such intriguing case is Stove Kraft Limited, a leading kitchen appliances company that has recently sparked the interest of investors.

On one side, the company boasts an established brand, a diverse product range, and expanding distribution network, making it an appealing opportunity for those looking to invest in the kitchen appliances market. On the other hand, decreasing institutional holding and negative profit after tax raise valid concerns that require careful evaluation.

To learn more about stock market basics and stock analysis one can consider enrolling in our Stock Market Learning Courses, here.

In this journey, we delve into Stove Kraft’s strengths and weaknesses, unravel the mysteries of its financial performance, and weigh the potential risks and rewards associated with investing in this kitchen appliances giant.

Our aim is to equip you with insights and understanding, empowering you to make informed decisions amidst today’s ever-changing investment landscape.

Let’s navigate through this investment dilemma together!

Company Overview:

Founded in 1999 by Rajendra Gandhi and Sunita Gandhi, Stove Kraft Limited is a renowned Indian kitchen appliances company with its headquarters in Bengaluru, India.

Stove Kraft specializes in the manufacturing, marketing, and distribution of high-quality kitchen appliances that cater to the diverse needs of Indian households.

Stove Kraft operates two state-of-the-art manufacturing units, located in Bangalore and Baddi. With a combined production capacity of 56 million units per annum, the company ensures a steady supply of its high-quality products.

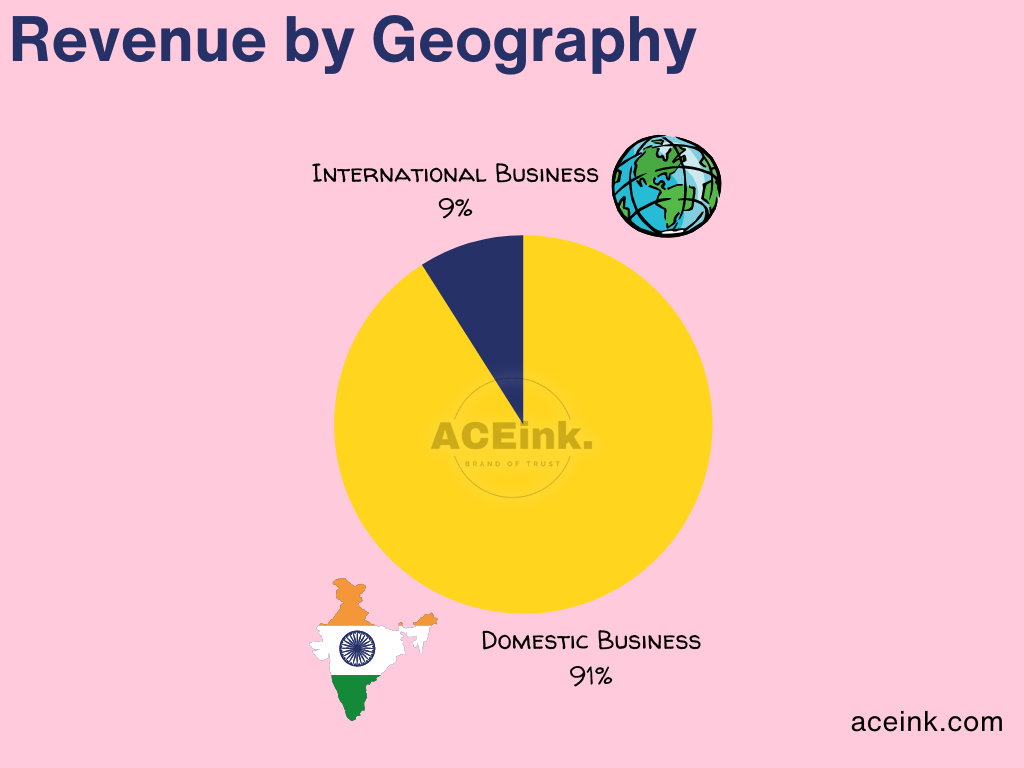

Over the years, it has earned a strong reputation as a trusted brand in the kitchen appliance industry, both domestically and internationally.

Stove Kraft’s Pigeon products have garnered popularity in 12 countries, and the company proudly serves as a vendor to renowned companies like Walmart Inc in the USA and Mexico.

Product Overview:

- LPG Gas Stoves: Stove Kraft’s flagship product, LPG gas stoves, offers a wide range of burner configurations and ergonomic designs, ensuring durability and efficiency.

- Chimneys: The company manufactures kitchen chimneys equipped with advanced filtration technology, effectively eliminating smoke, odors, and pollutants while adding an elegant touch to the kitchen.

- Cookware and Kitchen Tools: Stove Kraft provides precision-crafted cookware, pressure cookers, non-stick pans, tawas (flat griddles), and kitchen utensils, enhancing the overall cooking experience.

- Small Appliances: Stove Kraft offers an array of small kitchen appliances, such as toasters, sandwich makers, electric kettles, and mixer grinders, which simplify cooking tasks and improve kitchen efficiency.

- Modular Kitchen Solutions: Venturing into modular kitchen solutions, Stove Kraft offers kitchen cabinets, countertops, and storage solutions that optimize space utilization and create functional and elegant kitchens.

Acquisition of Skava Electric Private Limited:

In a strategic move, Stove Kraft is in the process of acquiring Skava Electric Pvt Ltd on a slump sale basis.

This venture enables the company to expand its product offering to include low-voltage switchgear solutions, encompassing electrical switches, sockets, distribution boards, switchboards, MCBs, bulb holders, and more.

The acquisition synergizes well with the existing Pigeon LED product range.

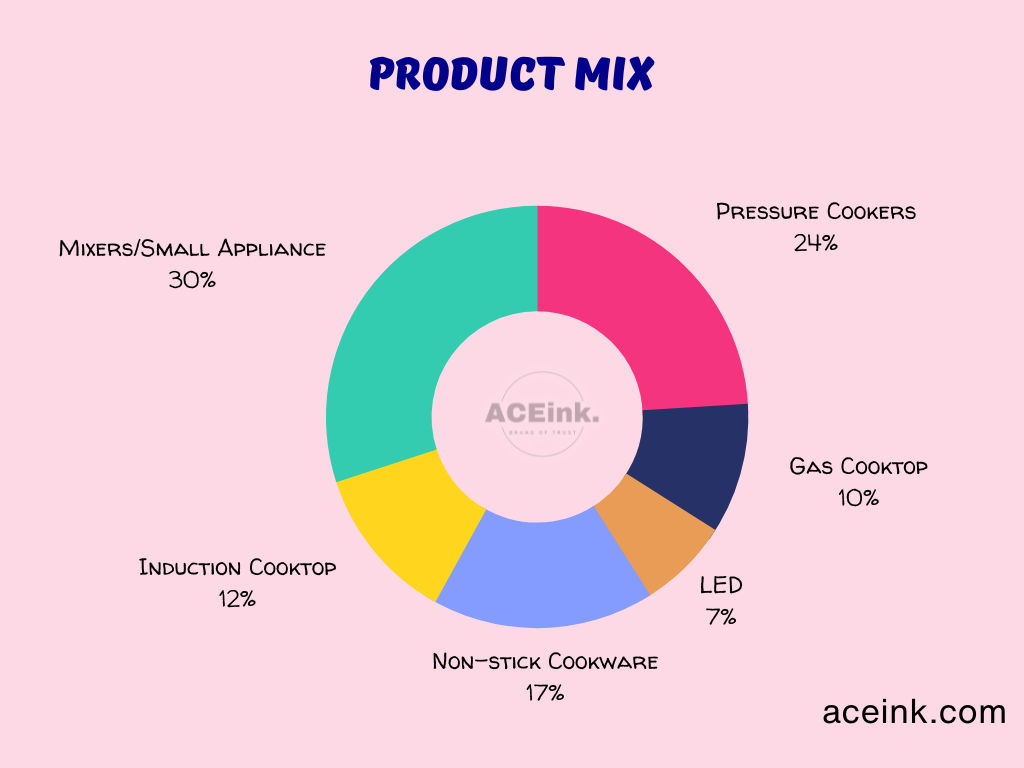

Product Performance:

Stove Kraft witnessed remarkable volume growth across all product categories, ranging from 8% to 16%. Specific product-wise volume growth percentages were as follows:

- Pressure Cooker – 19.6%

- Non-Stick Cookware – 16.8%

- Induction Cooktops – 13.4%

- Gas Cooktops – 4.3%

- Small Appliances – 11.1%

- While LED sales grew by 2.1% for the year, the overall product performance showcased encouraging results.

Financial Performance:

In FY’23, Stove Kraft experienced impressive growth:

- Revenue increased by 13% to INR 1,284 crores.

- EBITDA witnessed a growth of 4.4%.

- However, profit after tax for Q4 FY’23 reported a negative INR 6 crores.

- Key Ratio:

- ROCE 12.6 %

- ROE 9.32 %

- OPM 7.76 %

- Debt ₹ 163 Cr.

- Debt to equity 0.40

- Int Coverage 3.68

- Qtr Profit Var 1.49 %

- Qtr Sales Var 8.25 %

- Free Cash Flow ₹ -21.3 Cr.

Fundamentals:

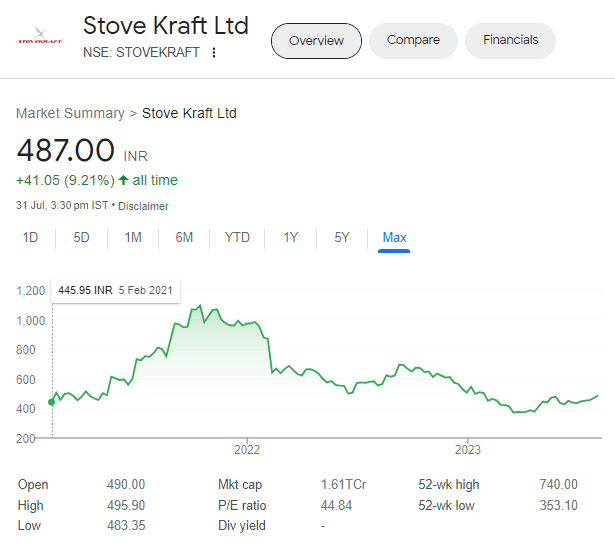

- Market Cap ₹ 1,610 Cr.

- Current Price ₹ 487

- High / Low ₹ 740 / 353

- Face Value ₹ 10.0

- Book Value ₹ 122

- Dividend Yield 0.00 %

- Stock P/E 44.9

- Industry PE 49.3

- PEG Ratio 1.15

- Return over 1year-16.5 %

Shareholding pattern:

- Promoter holding 55.9 %

- Change in Prom Hold 0.00 %

- FII holding 0.98 %

- Chg in FII Hold -2.18 %

- DII holding 1.15 %

- Chg in DII Hold -5.53 %

- Public holding 42.0 %

Capex:

Stove Kraft allocated INR 75 crores towards capex in the fiscal year, with an additional INR 20 crores set aside for future spending.

The company adheres to a capex limit of 25% of PAT along with depreciation and aims to set up a foundry for cast iron cookware.

Due to challenging market conditions, some of the planned capex for FY ’24 will be staggered to early FY ’25.

Strengths:

Strong Market Presence:

Stove Kraft has established itself as a leading player in the Indian kitchen appliances industry, commanding a significant market share. The company’s flagship product, LPG gas stoves, holds a dominant position in the market, with an impressive sales volume of over 3 million units annually.

This market dominance positions Stove Kraft as a trusted and reliable brand, providing a competitive advantage over its peers.

Diverse Product Range:

Stove Kraft’s extensive product portfolio offers a diverse range of kitchen appliances, catering to a wide spectrum of consumer needs.

The company’s chimneys have witnessed a remarkable growth rate of 20% YoY, driven by their advanced filtration technology and sleek designs, making them popular among Indian households.

Additionally, the growing demand for modular kitchen solutions presents significant growth opportunities for Stove Kraft.

Strong Distribution Network:

Stove Kraft’s well-established distribution network plays a crucial role in its success.

The company’s products are available in over 79,000 retail outlets, spanning both urban and rural areas across India.

Margins and ROE:

Stove Kraft has taken significant strides in improving its gross margins, recording an enhancement of 0.8%, with further anticipated growth of 1% in the current year.

The company targets a gross margin of 33.5% under normal circumstances, with 33% being the minimum acceptable threshold.

To achieve a 20% return on capital employed (ROCE), Stove Kraft aims to raise gross margins by at least 1% over the base of the last year.

While the investor emphasizes protecting margins over increasing market share, certain categories may witness price hikes to safeguard margins.

Stove Kraft remains steadfast in preserving margins and ROE even in challenging market conditions, and it exudes confidence in achieving a gross margin of at least 33.5%.

Amid its growth journey, Stove Kraft has successfully completed hiring for all new positions and has recently added two independent directors to its Board.

Retail Expansion:–

In the realm of retail expansion, Stove Kraft successfully added 54 stores in southern markets, setting its sight on further accelerating store reach in FY’24.

The company aims to establish approximately 100 new stores this year, at a rate of 7-8 stores per month.

The retail stores boast a gross margin of 45-48%, with costs ranging from INR 1.25 lakhs to INR 3 lakhs, generating an average monthly revenue of INR 4 lakhs.

Profits are typically achieved after the third month of operation.

Specific Risks Involved:

Conclusion:

Stove Kraft demonstrates both positive and negative aspects in its fundamental analysis. The company enjoys an established brand, a growing distribution network, an international presence, and a diverse product range.

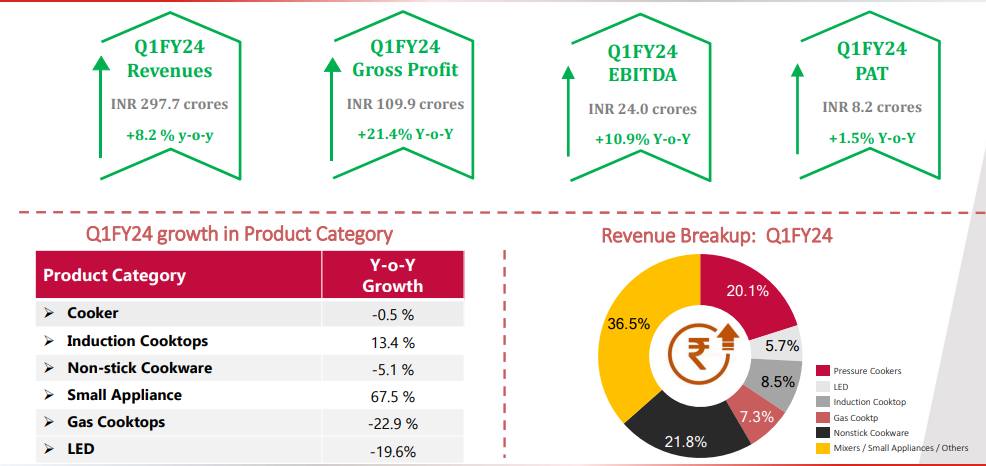

However, the decreasing institutional holding and negative PAT in the past raise concerns and require further scrutiny. On the positive side, the recent Q1 FY24 results show revenue growth and gross margin improvement, signaling progress in the company’s financial performance.

While Stove Kraft has promising aspects, it is vital to be cautious and understand the underlying factors driving its financial performance. Diversification and risk management remain essential components of a well-rounded investment strategy.

Please note that we are not SEBI-registered advisors or analysts. All the views shared in this article and all the content shared on aceink.com are only for learning and educational purposes. Any part of the article or any information on Aceink.com should not be interpreted or considered as investment advice. None of the opinions, views, or content posted on Aceink.com constitutes investment advice, as we are not SEBI-registered advisors or analysts.

DISCLAIMER:

We are not SEBI-registered advisors or analysts. All the views shared in this article and all the content shared on aceink.com are only for learning and educational purposes. Any part of the article or any information on Aceink.com should not be interpreted or considered as investment advice. None of the opinions, views, or content posted on Aceink.com constitutes investment advice, as we are not SEBI-registered advisors or analysts.

Aceink.com or any person associated with this website accepts no liability or responsibility for any direct, indirect, implied, or any other consequential damages arising directly or indirectly due to any action taken based on the information provided on this website. Please conduct your own research, and we suggest seeking investment advice only from a SEBI-registered investment advisor.

The views expressed by investment experts, broking houses, news and media houses, rating agencies, etc., are their own and not those of Aceink.com or its management. Aceink.com advises users to consult a SEBI-registered investment advisor before making any decisions.

——————

Ethanol blending is a great innovation will it cut retail prices so drastically? “All the vehicles will now…Read More