“What’s driving Kirloskar Brothers’ unprecedented growth?”

On Friday’s intra-day trade on the Bombay Stock Exchange (BSE), Kirloskar Brothers Limited (KBL) experienced a surge of 9% in its shares, driving the price up to Rs 418. This increase in share price can be attributed to the company’s positive business outlook, and experts predict that the growth stock can reach its 52-week high of Rs 424, which was achieved on November 25, 2022.

KBL is a prominent member of the Kirloskar Group and is known for its expertise in fluid management.

Also Read: Why This Fundamentally Strong EV Stock is on a Bullish Run in a Bear Market?

About Kirloskar Brothers Limited (KBL)

-Leading Indian multinational company that specializes in the engineering and manufacturing of fluid management solutions.

-Established in 1888, the company has been providing top-notch products and services for over 135 years.

-It has its registered office located in Maharashtra, and

-6 manufacturing units in India, and

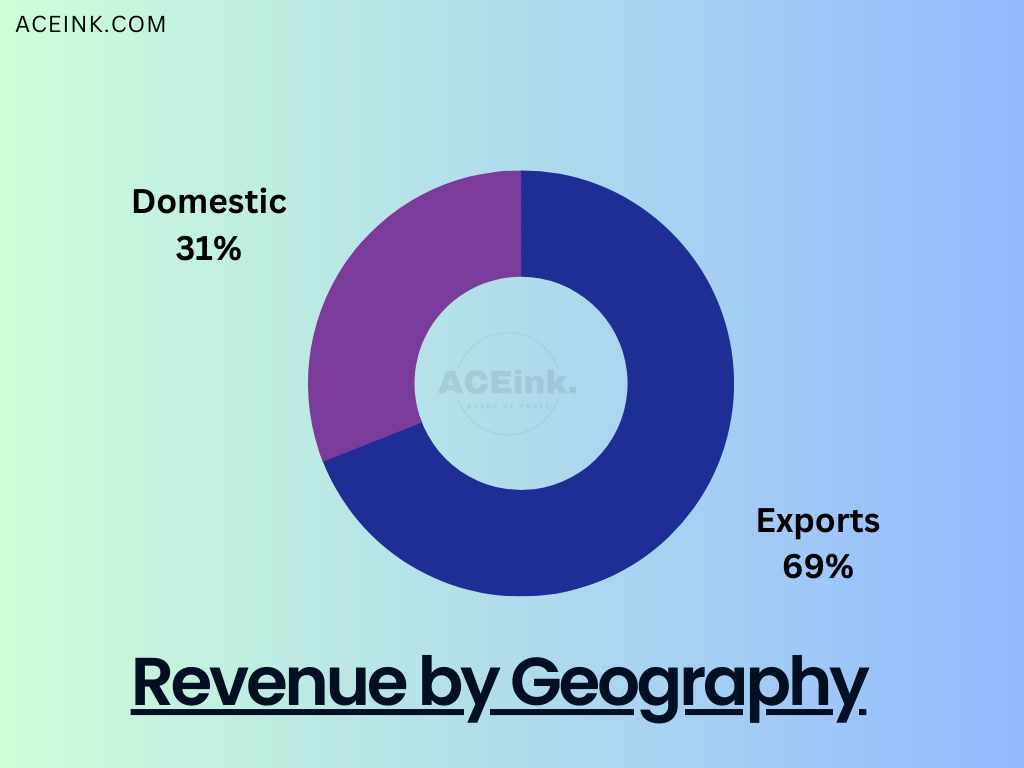

-5 units globally, catering to 6 Continents & 100+ Countries

– with a diversified product range of 250+ products and 1,00,000+ SKUs

The company offers comprehensive solutions for fluid management on large infrastructure projects, such as

-water supply,

-power plants,

-irrigation,

-oil and gas,

-marine and defense.

It designs and manufactures pumps, valves, and hydro turbines that are used in a variety of industrial, agricultural, and domestic applications.

The ASME Acknowledgment

-KBL has been acknowledged for its exceptional pump manufacturing capabilities by the American Society of Mechanical Engineers (ASME), which has awarded the company the N and NPT certification.

-This accolade is a testament to the company’s engineering and manufacturing prowess, and

KBL is the only pump manufacturing company in India and the ninth in the world to receive this distinction.

Reason for Growth

Focus on research and development:

-Kirloskar Brothers has a strong focus on research and development, which enables it to innovate and develop new products and solutions. This focus on R&D helps the company stay ahead of the competition and provide its customers with cutting-edge solutions that meet their evolving needs.

-The company’s R&D expense (23 crores) contributed 0.7% of the total revenue.

Strategic partnerships and collaborations:

-Collaborated with the Indian Institute of Technology, Bombay, to develop new technologies for water and energy management. These partnerships and collaborations can help Kirloskar Brothers access new markets, develop new products, and improve its overall competitiveness.

-The Co also has strategic global partnerships with Reliance Industries, ArcelorMittal, Hyundai Engineering, NTPC, Linde, Saudi Aramco, Nuclear power corporation of India, Hitachi, etc

Growing demand for water and energy management solutions:

-As global populations grow, the demand for water and energy management solutions is increasing.

-The company’s expertise in fluid management and its diversified product portfolio makes it an attractive partner for businesses looking to improve their water and energy management.

Focus:

-Over the years, the company has shifted its focus away from the low-margin and working capital-intensive EPC business towards services and value-added products.

-This strategic shift is reflected in the declining share of EPC business in revenues, which has decreased from 75% in FY10 to 6% in FY22

Strong financial performance:

-In Q3FY23 (October-December quarter), KBL launched new products such as the KW series vertical pump for HVAC applications and a submersible borewell pump capable of handling sand particles and low energy consumption

-During the first nine months of the current financial year 2022-23 (April-December), Kirloskar Brothers Limited (KBL) reported a consolidated profit after tax (PAT) of Rs 135.10 crore, more than double the PAT of Rs 39.7 crore in the corresponding period of the previous year, owing to strong operational performance.

-KBL’s revenue for the same period grew 23.9% YoY to Rs 2,606 crore, up from Rs 2,103 crore in the previous year, with an EBITDA margin improvement of 362 basis points (bps) to 10.3%.

-This margin improvement can be attributed to an enhanced product mix, operating leverage, and revenue recognition from a high-value order.

– Additionally, KBL’s consolidated order book saw a YoY growth of 21% to reach Rs 2,845 crore.

Attractive valuation:

-currently trading at a Cheaper valuation, with a P/E ratio of around 17, compared to the industry average of around 23. This provides investors with an opportunity to invest in a high-quality company at a reasonable price.

Kirloskar Brothers Ltd has a history of strong financial performance. The company’s revenue has grown consistently over the years, and it has maintained a healthy balance sheet with manageable debt levels. This financial stability makes Kirloskar Brothers a less risky investment option compared to companies with high debt levels or inconsistent financial performance.

——————–

This electric vehicle EV stock is on the rise to reach an all-time high (ATH) in the current falling market. Here is the reason why…Read More

“Why This Fundamentally Strong EV Stock is on a Bullish Run in a Bear Market?”

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies are their own and not that of the website or its management. Aceink.com advises users to check with certified experts before taking any investment decisions.